Medicare Part D is the federal program that provides prescription drug coverage to over 51.5 million Medicare beneficiaries. Today, 92% of all prescriptions filled under Part D are generics, but many people don’t know how these drugs are covered or why costs vary so much between plans. This guide breaks down exactly how generic drug coverage works in 2026, with clear rules, current costs, and practical steps to save money.

What exactly is a Medicare Part D formulary?

A formulary is simply a list of drugs a Part D plan covers. Each plan must follow strict rules from the Centers for Medicare & Medicaid Services (CMS). For example, every plan must cover at least two different generic versions of drugs in each therapeutic class (like blood pressure or diabetes medications). CMS also requires plans to cover 85% of drugs in each category, including generics. The goal is to ensure you have access to affordable options while keeping costs manageable for the program.

How generics fit into Part D’s tier system

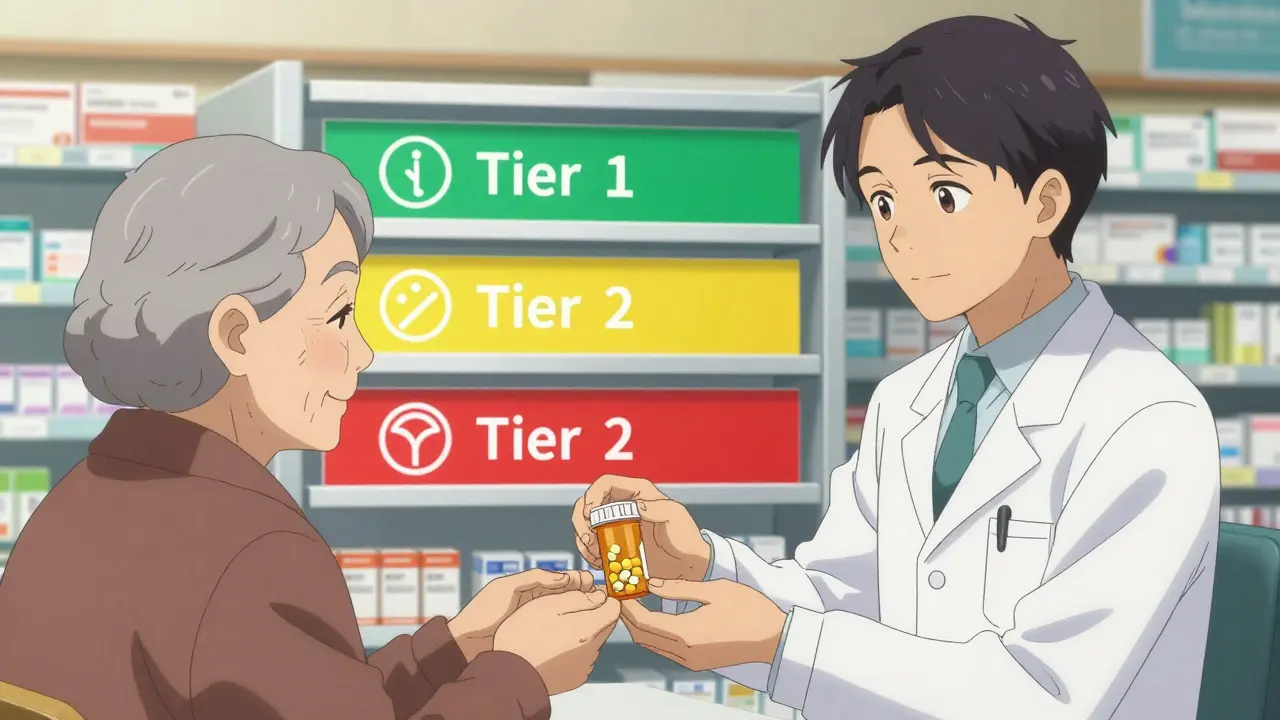

Part D plans organize drugs into tiers based on cost. Generics usually sit in the lowest tiers, where you pay less. Here’s how it breaks down for 2026:

| tier | generic drugs covered | typical cost |

|---|---|---|

| Tier 1 | Preferred generics | $0-$15 copay for 30-day supply |

| Tier 2 | Non-preferred generics | 25% coinsurance or $15-$40 copay |

| Tiers 3-5 | Brand-name drugs (rarely generics) | $40-$100+ copay or higher coinsurance |

Most generic drugs you take daily-like metformin for diabetes or lisinopril for blood pressure-fall into Tier 1. These are the cheapest options. If your plan only covers one generic version of a drug, you might pay more for alternatives. For example, if your plan covers only amlodipine (a common blood pressure generic) but not nifedipine, you’d pay full price for nifedipine even if it’s equally effective.

How your out-of-pocket costs work in 2026

Part D has four cost phases. For generics, the math is simpler than for brand-name drugs:

- Deductible phase: You pay 100% of costs until you hit the $615 deductible (same as 2025). Some plans have a $0 deductible for generics-check yours.

- Initial coverage phase: After meeting the deductible, you pay 25% of the drug’s cost for generics. For example, a $30 Tier 1 generic would cost you $7.50. This phase continues until your total out-of-pocket hits $2,100.

- Catastrophic coverage phase: Once you hit $2,100 in out-of-pocket costs (up from $2,000 in 2025), you pay $0 for generics for the rest of the year. This is a huge change from the "donut hole" era.

- Out-of-pocket cap: The Inflation Reduction Act’s $2,100 cap for 2026 means no more unexpected spikes in drug costs. This alone saves the average beneficiary $450 yearly on generics.

One key detail: only what you pay counts toward the $2,100 cap for generics. For brand-name drugs, 70% of the drug’s total cost counts toward the cap. This is why sticking to generics lowers your out-of-pocket costs faster.

How the Inflation Reduction Act changed generic coverage

Passed in 2022, this law made major changes effective January 2025. For 2026, the biggest impacts are:

- No more "donut hole" gap: Before 2025, there was a coverage gap where you paid 25% for generics. Now, after the deductible, you pay only 25% until hitting the $2,100 cap.

- Lower costs in catastrophic phase: Medicare now covers 100% of generic costs after you hit the cap. Before, you paid 5%.

- Price negotiations for generics: Starting in 2029, CMS will negotiate prices for some generics (like insulin glargine). This could drop costs even further.

These changes mean you’ll pay less overall. For example, if you take three Tier 1 generics costing $10 each monthly, you’d pay $7.50 per month in the initial phase. After hitting the $2,100 cap, those same drugs cost you $0. Before the Inflation Reduction Act, you’d have paid 25% during the donut hole phase-adding up to hundreds more yearly.

How to find the best Part D plan for your generics

Not all plans cover the same generics. Here’s how to compare them:

- Use the Medicare Plan Finder tool: Enter your specific medications (e.g., "metformin 500mg") and zip code. The tool shows which plans cover them at the lowest tier.

- Check the Annual Notice of Change (ANOC): Every fall, your plan sends this letter. It lists changes to your drug coverage for next year. If a generic you take moves to a higher tier, consider switching plans.

- Ask about generic substitution policies: Some plans allow pharmacists to switch between generics in the same class. For example, if your plan covers atorvastatin but not simvastatin, the pharmacist might substitute one for the other. Always confirm with your pharmacist.

- Request a coverage determination: If your plan doesn’t cover a needed generic, you can appeal. CMS data shows 83% of these requests are approved. Call 1-800-MEDICARE or visit Medicare.gov for help.

Many beneficiaries save $400+ yearly by switching plans based on generic coverage. For instance, a 2026 KFF analysis found that 61% of people who used the Plan Finder tool saved an average of $427 annually by choosing a plan with better generic tiers.

Common problems and how to fix them

Even with good rules, issues arise. Here’s what to watch for:

- "Therapeutic interchange" problems: If your plan covers one generic but not another in the same class (e.g., furosemide vs. torsemide), you might pay full price for the non-covered version. Talk to your doctor about switching to a covered drug.

- Formulary changes: 37% of Part D plans change at least one generic’s tier each year. Review your ANOC carefully before open enrollment.

- Pharmacy issues: Some pharmacies don’t stock certain generics. Call ahead or ask your pharmacist to order it. If they refuse, contact your plan for assistance.

Reddit users often share these frustrations. One user, "MedicareVeteran82," reported being charged full price for a generic blood pressure medication because their plan only covered a different generic in the same class. Another user, "SmartSenior2024," praised their plan for covering three heart medications at $0 under Tier 1-saving over $300 monthly.

FAQ: Medicare Part D generic coverage

What’s the difference between Tier 1 and Tier 2 generics?

Tier 1 generics are "preferred" drugs with the lowest copays (usually $0-$15). Tier 2 generics are "non-preferred" and cost more-either 25% coinsurance or a $15-$40 copay. For example, a Tier 1 generic like lisinopril might cost $5, while a Tier 2 generic like hydrochlorothiazide could cost $20. Always check which tier your specific drug falls into.

Does the $2,100 out-of-pocket cap apply to all generics?

Yes. Once you hit $2,100 in out-of-pocket costs for the year (including what you pay for all drugs), you enter catastrophic coverage. From there, you pay $0 for all generics (and most brand-name drugs) for the rest of the year. This cap applies to all Part D plans in 2026.

Can I switch plans if my generic isn’t covered?

Absolutely. You can change plans during the Annual Enrollment Period (October 15-December 7) or during Special Enrollment Periods. If your current plan doesn’t cover a generic you need, file a coverage determination request. If denied, you can appeal. Most appeals succeed-83% of requests get approved according to CMS data.

Why do some plans cover one generic but not another?

Plans choose which generics to cover based on cost and effectiveness. For example, a plan might cover atorvastatin but not pravastatin because atorvastatin is cheaper. This is allowed under CMS rules as long as at least two generics are available in the class. If your specific drug isn’t covered, ask your doctor about alternatives or request an exception.

How do I know if my plan covers a specific generic?

Use the Medicare Plan Finder tool at Medicare.gov. Enter your medication name and dosage. It will show which plans cover it and at what tier. You can also check your plan’s formulary online or call customer service. Always verify before enrolling-37% of plans change generic coverage yearly.

Next steps for 2026

By now, you should know how Part D covers generics and how to save money. Here’s what to do next:

- Review your ANOC: If you’re already enrolled, check your Annual Notice of Change letter. Look for changes to your generics’ tiers or coverage.

- Compare plans: Use the Medicare Plan Finder tool before open enrollment (October 15-December 7) to find the best plan for your medications.

- Ask questions: If you’re unsure, call 1-800-MEDICARE or visit Medicare.gov. The Medicare Rights Center also offers free counseling at medicarerights.org.

Remember: generics save you money, but only if your plan covers them. Taking a few minutes to check your coverage could save hundreds this year.

Sam Salameh

The $2,100 out-of-pocket cap is a game-changer for seniors on Medicare Part D. I've helped my mom navigate the system for years, and this change alone saves her hundreds each year. Generics in Tier 1 are the way to go-cheaper and just as effective. America's healthcare system is still the best, but we need to keep improving access. Let's make sure everyone gets the care they need without breaking the bank.

Cole Streeper

The government says it's a cap, but they'll change it next year. Always happens. They want to keep us in the dark about how much drugs really cost. I've got my sources saying this is just a trick to get us to buy more expensive brands. Don't trust them!

Dina Santorelli

Let me break this down: the tier system is a joke. Tier 1 generics are only covered if you're lucky. Most plans don't actually have them. And that $2,100 cap? It's a mirage. They'll find a way to claw it back. I've been doing this for years, and it's always worse than they say.

Katharine Meiler

The formulary structure is designed to balance access and cost-effectiveness. For instance, Tier 1 preferred generics typically have lower copays due to negotiated rebates. However, the non-preferred generics in Tier 2 often have higher coinsurance, which can impact out-of-pocket expenses. It's crucial to review the specific plan's formulary to optimize coverage. This ensures you're getting the best value for your medications.

Danielle Vila

They're hiding something! All these 'generics' are just rebranded brand names with cheaper ingredients. The FDA and CMS are in cahoots to make us think we're saving money. I've seen the documents-these drugs are barely different. And that $2,100 cap? It's a trap. Next year it'll be $5,000. Mark my words.

Thorben Westerhuys

Oh my goodness!!! The $2,100 cap is such a relief!!! I can't believe how much I've saved on my meds!!! It's just incredible-so many seniors are struggling, but this change is life-changing!!! I'm so grateful for the Inflation Reduction Act!!! It's truly a blessing!!! 🙏🙏🙏

Laissa Peixoto

The key to understanding Part D is recognizing that generics are the backbone of affordable coverage. By focusing on Tier 1 drugs, beneficiaries can minimize costs. It's not just about the numbers-it's about ensuring people can access necessary medications without financial strain. A system that prioritizes health over profit is a system worth supporting. This change is a step in the right direction. Let's not forget the history of Part D and how it's evolved. When it was first introduced, many seniors struggled with coverage gaps. The donut hole was a nightmare for those on chronic medications. But with the Inflation Reduction Act, things have changed dramatically. The $2,100 cap means no more unexpected spikes in costs. This is a huge relief for millions. Generics play a critical role here-they're cheaper and just as effective as brand names. Understanding the tier system is key to maximizing savings. For example, Tier 1 generics often have $0-$15 copays, while Tier 2 might be higher. It's important to check your specific plan each year. Formularies change frequently, and what was covered last year might not be this year. By staying informed, you can avoid costly surprises. This is why tools like the Medicare Plan Finder are invaluable. They help you compare plans based on your specific medications. Don't wait until the last minute-review your coverage during open enrollment. Taking these steps now can save you hundreds next year. It's all about proactive planning.

one hamzah

This is awesome! 😊 Generics save so much money! I've been using Part D for years and the $2100 cap is a game changer! 🌟 People in developing countries need this too!

Joyce cuypers

I'm so happy about the new cap! It's going to help so many people! My cousin just started taking meds and this will make a huge differnce! I'm so proud of the progress we're making! 🎉

Georgeana Chantie

This is all a joke. The government keeps promising savings, but prices keep rising. We need to take back control of our healthcare. Stop relying on federal programs-private insurance is better. Always has been. They don't care about us.

Carol Woulfe

The so-called 'cap' is merely a facade.

Lisa Scott

They say it's a cap but it's just a trick.

Brendan Ferguson

The changes to Part D are a step in the right direction. By focusing on generics and capping out-of-pocket costs, we're making healthcare more accessible. It's important to stay informed and advocate for further improvements. Let's keep working together to make sure everyone gets the care they need. This is progress worth celebrating.